REFUND OF TAXES IN G.R. NO. 271261

Adding to the wealth of jurisprudence in interpreting the two-year prescriptive period, the Supreme Court revisited the interpretation of the two-year prescriptive period for tax refund claims under Section 229 of the National Internal Revenue Code, as amended in its decision in G.R. No. 271261. The central issue in this case was the proper reckoning point for the two-year prescriptive period and what constitutes “payment of taxes.”

In this case, the petitioner is a corporation engaged in developing and operating tourist facilities such as casino entertainment complexes with hotels, retail, and amusement areas. It has a valid and existing gaming license issued by the Philippine Amusement and Gaming Corp. (PAGCOR). The petitioner paid taxes to the BIR, claiming that they had “erroneously or illegally collected and passed on input VAT on purchases attributable to gaming revenue.” Thereafter, the petitioner filed an application for a refund with the BIR, which was then denied.

In summary of the proceedings, the claim of refund under Sec. 112 of the Tax Code of the Petitioner failed in the Court of Tax Appeals (CTA) as well as with the Supreme Court. The Supreme Court agrees that while the petitioner is a VAT-exempt entity under special laws, its transactions with suppliers are not considered zero-rated or effectively zero-rated sales under the Tax Code. In the case, the CTA sitting en banc concluded that since the petitioner was seeking the refund of its “erroneous payment of passed-on input VAT on purchases” attributable to gaming revenue for the first quarter of 2016, the applicable provision is Section 229 of the Tax Code for recovery of taxes erroneously paid.

As such, one of the primordial issues raised in the case before the Supreme Court is the interpretation of the phrase “payment of taxes” under Section 229. The petitioner argued that this should be interpreted “as the time the passed-on taxes” are determined to be erroneous, which is the date of the filing of the quarterly VAT return declaring the input VAT subject to the claim for refund. In contrast, the CTA en banc held that the two-year period should be counted from the actual date of payment to the BIR of the VAT passed on to the Petitioner by its suppliers and that the operative act under Section 229 of the Tax Code is the “actual remittance by the supplier.”

In resolving the dispute, the Supreme Court reaffirmed its established jurisprudence on the matter. It emphasized that the phrase “payment of taxes” under Section 229 is to be interpreted in two ways: (1) the actual payment of tax or penalty sought to be refunded, regardless of the existence of any supervening cause after payment, as well as (2) the date of filing of the adjusted final tax return. The court did not require “actual remittance by the suppliers” as the reckoning point. By applying the principle of “substantial justice, equity, and fair play” the court ruled that the actual date of filing of the quarterly VAT return of petitioner should be the reckoning point.

The court clarified that for income tax refunds, the two-year period begins from the filing of the Final Adjustment Return and not when the quarterly income tax was paid. The court established that only on the Final Adjustment Return is when the taxpayer’s actual tax liability or overpayment can be determined. Likewise, the court ruled that the prescriptive period starts from the filing of the adjusted final tax return, which reflects the audited and finalized figures of the taxpayer’s operations. Lastly, the court maintained that it has not required “actual remittance by the suppliers” as the reckoning point; rather, it has consistently reckoned the two-year prescriptive period from the actual payment of tax or penalty sought to be refunded as well as on the date of filing of the adjusted final tax return.

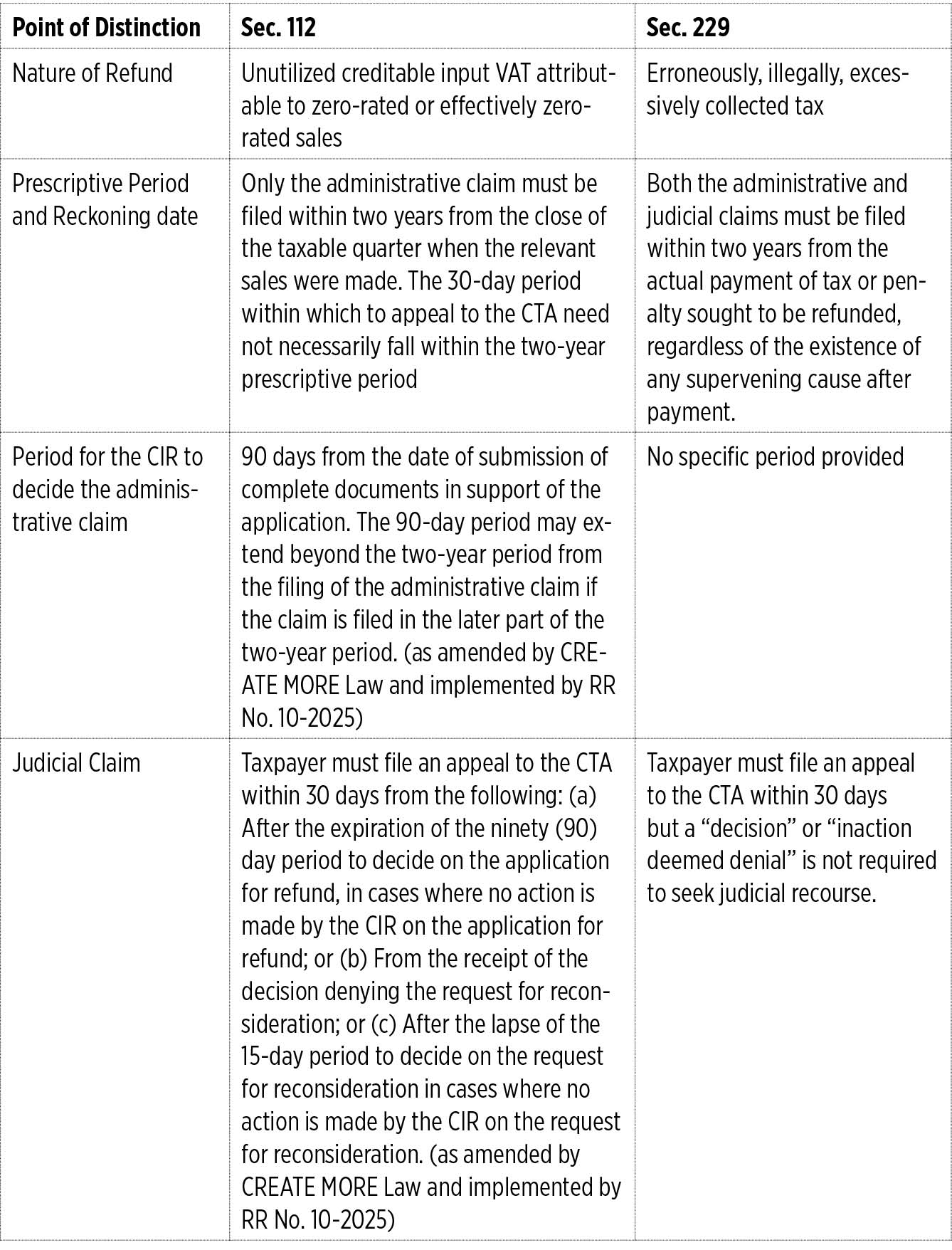

DIFFERENCES BETWEEN SECTIONS 112 AND 229

It must be noted that the petitioner applied for relief with the Court for the application of both Section 112 and Section 229 of the Tax Code. Section 112 pertains to the refund of unutilized creditable input VAT attributable to zero-rated or effectively zero-rated sales. Section 229 pertains to refund of taxes alleged to have been erroneously or illegally assessed or collected, or claimed to have been collected without authority. After all, the amount being refunded herein pertains to “collected and passed-on input VAT on purchases attributable to gaming revenue.” Eventually, the Court ultimately decided that it is Section 229 (for erroneously, illegally, excessively paid and collected taxes) that is the applicable legal basis in this case and disagreed that Section 112 (for refund of unutilized input VAT) is applicable.

To summarize the difference, as presented in the case above, here are the distinctions between Sections 112 and 229 (see table).

IN SUMMARY

The court’s ruling in G.R. No. 271261 adds clarity to the interpretation of the two-year prescriptive period for tax refund claims under Section 229. By reaffirming that the reckoning point may be either the actual payment of the tax or the filing of the adjusted final tax return, the court underscores its commitment to substantial justice and equitable treatment of taxpayers. This decision not only harmonizes previous jurisprudence but also delineates the boundaries between claims under Sections 229 and 112, providing clearer guidance for taxpayers navigating the complexities of applications for claims for refund of taxes. As tax laws continue to evolve, the decision serves as a timely reminder of the importance of precision in statutory interpretation and the enduring role of jurisprudence in shaping tax administration.

Let’s Talk Tax is a weekly newspaper column of P&A Grant Thornton that aims to keep the public informed of various developments in taxation. This article is not intended to be a substitute for competent professional advice.

John Patrick L. Paumig is a manager of the Tax Advisory & Compliance division of P&A Grant Thornton, the Philippine member firm of Grant Thornton International Ltd.

business.development@ph.gt.com